Oct 06, 2019

Suppose you observe the historical returns of $p$ different fund managers,

and wish to test whether any of them have superior Signal-Noise ratio (SNR)

compared to the others.

The first test you might perform is the test of pairwise equality of all SNRs.

This test relies on the multivariate delta method and central limit theorem,

resulting in a chi-square test, as described by Wright et al and outlined

in section 4.3 of our Short Sharpe Course.

This test is analogous to ANOVA, where one tests different populations for unequal

means, assuming equal variance.

(The equal Sharpe test, however, deals naturally with the case of paired observations,

which is commonly the case in testing asset returns.)

In the analogous procedure, if one rejects the null of equal means in an ANOVA, one

can perform pairwise tests for equality. This is called a post hoc test, since

it is performed conditional on a rejection in the ANOVA.

The basic post hoc test is Tukey's range test, sometimes called 'Honest Significant Differences'.

It is natural to ask whether we can extend the same procedure to testing the SNR.

Here we will propose such a procedure for a crude model of correlated returns.

The Tukey test has increased power by pooling all populations together to

estimate the overall variance. The test statistic then becomes something like

$$

\frac{Y_{(p)} - Y_{(1)}}{\sqrt{S^2 / n}},

$$

where $Y_{(1)}$ is the smallest mean observed, and $Y_{(p)}$ is the largest,

and $S^2$ is the pooled estimate of variance. The difference between

the maximal and minimal $Y$ is why this is called the 'range' test,

since this is the range of the observed means.

Switching back to our problem, we should not have to assume that our

tested returns series have the same volatility.

Moreover, the standard error of the Sharpe ratio is only weakly dependent

on the unknown population parameters, so we will not pool variances.

In our paper on testing the asset with maximal Sharpe,

we established that the vector of Sharpes, for normal returns and

when the SNRs are small,

is approximately asymptotically normal:

$$

\hat{\zeta}\approx\mathcal{N}\left(\zeta,\frac{1}{n}R\right).

$$

Here $R$ is the correlation of returns.

See our previous blog post for more details.

Under the null hypothesis that all SNRs are equal to $\zeta_0$,

we can express this

$$

z = \sqrt{n} \left(R^{1/2}\right)^{-1} \left(\hat{\zeta} - \zeta_0\right) \approx\mathcal{N}\left(0,I\right),

$$

where $R^{1/2}$ is a matrix square root of $R$.

Now assume the simple rank-one model for correlation, where

assets are correlated to a single common latent factor,

but are otherwise independent:

$$

R = \left(1-\rho\right) I + \rho 1 1^{\top}.

$$

Under this model of $R$ we computed inverse-square-root

of $R$ as

$$

\left(R^{1/2}\right)^{-1} = \left(1-\rho\right)^{-1/2} I + \frac{1}{p}\left(\frac{1}{\sqrt{1-\rho+p\rho}} - \frac{1}{\sqrt{1-\rho}}\right)1 1^{\top}.

$$

Picking two distinct indices, $i, j$ let $v = \left(e_i - e_j\right)$ be the contrast

vector. We have

$$

v^{\top}z = \frac{\sqrt{n}}{\sqrt{\left(1-\rho\right)}}v^{\top}\hat{\zeta},

$$

because $v^{\top}1=0$.

Thus the range of the observed Sharpe ratios is a scalar multiple of the range

of a set of $p$ independent standard normal variables.

This is akin to the 'monotonicity' principle that we abused earlier

when performing inference on the asset with maximum Sharpe.

Under normal approximation and the rank-one correlation model, we should then

see

$$

\left|\hat{\zeta}_{i} - \hat{\zeta}_{j}\right| \ge HSD = q_{1-\alpha,p,\infty} \sqrt{\frac{(1-\rho)}{n}},

$$

with probability $\alpha$, where the $q_{1-\alpha,m,n}$ is the upper $\alpha$-quantile

of the Tukey distribution with $m$ and $n$ degrees of freedom.

This is computed by qtukey in R.

Alternatively one can construct confidence intervals around each $\hat{\zeta}_i$ of

width $HSD$, whereby if another $\hat{\zeta}_j$ does not fall within it, the two

are said to be Honestly Significantly Different. The familywise error rate should be

no more than $\alpha$.

Testing

Let's test this under the null. We spawn 4 years of correlated returns

from 16 managers, then compare the maximum and minimum observed Sharpe ratio,

comparing them to the test value of $HSD$.

Assume that the correlation is known to have value $\rho=0.8$.

(More realistically, it would have to be estimated.)

Note that for this many fund managers we have

$$

q_{0.95,16,\infty}=4.85,

$$

and thus taking into account the $\sqrt{1-\rho}$ term,

$$

HSD = \frac{1}{\sqrt{n}} 2.17.

$$

This is only slightly bigger than the naive approximate confidence

intervals one would typically apply to the Sharpe ratio, which in this case

would be around

$$

\frac{\Phi^{-1}\left(0.975\right)}{\sqrt{n}} = \frac{1.96}{\sqrt{n}}.

$$

We perform 10 thousand simulations, computing the Sharpe over all managers,

and collecting the ranges. We compute the empirical type I error rate,

and find it to be nearly equal to the nominal value of 0.05:

suppressMessages({

library(mvtnorm)

})

nman <- 16

nyr <- 4

ope <- 252

SNR <- 0.8 # annual units

rho <- 0.8

nday <- round(nyr * ope)

R <- pmin(diag(nman) + rho,1)

mu <- rep(SNR / sqrt(ope),nman)

nsim <- 10000

set.seed(1234)

ranges <- replicate(nsim,{

X <- mvtnorm::rmvnorm(nday,mean=mu,sigma=R)

zetahat <- colMeans(X) / apply(X,2,sd)

max(zetahat) - min(zetahat)

})

alpha <- 0.05

HSDval <- sqrt((1-rho) / nday) * qtukey(alpha,lower.tail=FALSE,nmeans=nman,df=Inf)

mean(ranges > HSDval)

Compact Letter Display

The results of Tukey's test can be difficult to summarize. You might observe,

for example, that managers 1 and 2 have significantly different SNRs,

but not have enough evidence to say that 1 and 3 have different SNR, nor 2 and 3.

How, then should you think about manager 3? He/She perhaps has the same SNR as

2, and perhaps the same as 1, but you have evidence that 1 and 2 have different SNR.

You might label 1 as being among the 'high performers' and 2 among the 'average performers';

In which group should you place 3?

One answer would be to put manager 3 in both groups.

This is a solution you might see as the result of compact letter displays, which is

a commonly used way of communicating the results of multiple comparison procedures

like Tukey's test.

The idea is to put managers into multiple groups, each group identified by a letter,

such that if two managers are in a common group, the HSD test fails to find they

have significantly different SNR.

The assignment to groups is actually not unique, and so subject to

optimizing certain criteria, like minimizing the total number of groups, and so on,

cf. Gramm et al.

For our purposes here, we use Piepho's algorithm, which is conveniently provided

by the multcompView package in R.

Here we apply the technique to the series of monthly returns of 5 industry

factors, as compiled by Ken French, and published in his data library.

We have almost 1200 months of data for these 5 returns.

The returns are highly positively correlated, and we find that their

common correlation is very close to 0.8.

For this setup, and measuring the Sharpe in annualized units,

the critical value at the 0.05 level is

$$

HSD = \sqrt{12/n} 1.73.

$$

For comparison, the half-width of the two sided confidence interval on the

Sharpe in this case would be

$$

\sqrt{12/n} 1.96,

$$

which is a bit bigger. We have actually gained resolving power in our

comparison of industries because of the high level of correlation.

Below we compute the observed Sharpe ratios of the five industries,

finding them to range from around $0.49\,\mbox{year}^{-1/2}$ to

$0.67\,\mbox{year}^{-1/2}$.

We compute the HSD threshold, then call Piepho's method and

print the compact letter display, shown below.

In this case we require two groups, 'a' and 'b'.

Based on our post hoc test, we assign

Healthcare and Other into two different groups, but find no other

honest significant differences, and so Consumer, Manufacturing and Technology

get lumped into both groups.

# this is just a package of some data:

# if (!require(aqfb.data)) { install.packages('shabbychef/aqfb_data') }

library(aqfb.data)

data(mind5)

mysr <- colMeans(mind5) / apply(mind5,2,FUN=sd)

# sort decreasing for convenience later

mysr <- sort(mysr,decreasing=TRUE)

# annualize it

ope <- 12

mysr <- sqrt(ope) * mysr

# show

print(mysr)

## Healthcare Consumer Manufacturing Technology Other

## 0.6674 0.6487 0.5967 0.5906 0.4852

srdiff <- outer(mysr,mysr,FUN='-')

R <- cov2cor(cov(mind5))

# this ends up being around 0.8:

myrho <- median(R[row(R) < col(R)])

alpha <- 0.05

HSD <- sqrt(ope) * sqrt((1-myrho) / nrow(mind5)) * qtukey(alpha,lower.tail=FALSE,nmeans=ncol(mind5),df=Inf)

library(multcompView)

lets <- multcompLetters(abs(srdiff) > HSD)

print(lets)

## Healthcare Consumer Manufacturing Technology Other

## "a" "ab" "ab" "ab" "b"

Jun 04, 2019

In a previous blog post we used the

'Polyhedral Inference' trick of Lee et al. to perform

conditional inference on the asset with maximum Sharpe ratio.

This is now a short paper on arxiv.

I was somewhat disappointed to find, as noted in the paper,

that polyhedral inference has lower power than a simple Bonferroni correction

against alternatives where many assets have the same Signal-Noise ratio.

(Though apparently it has higher power when one asset alone higher SNR.)

The interpretation is that when there is no spread in the SNR, Bonferroni

correction should have the same power as a single asset test, while

conditional inference is sensitive to the conditioning information that

you are testing a single asset which has Sharpe ratio perhaps near that of

other assets. In the opposite case, Bonferroni suffers from having to 'pay'

for a lot of irrelevant (for having low Sharpe) assets, while conditional

inference does fine.

I also showed in the paper, as I demonstrated in a previous blog post,

that the Bonferroni correction is conservative when asset

returns are correlated. In a simple simulations under the null, I showed

that the empirical type I rate goes to zero as common correlation $\rho$ goes to one.

In this blog post I will describe a simple trick to correct for average positive

correlation.

So let us suppose that we observe returns on $p$ assets over $n$ days,

and that returns have correlation matrix $R$.

Let $\hat{\zeta}$ be the vector of Sharpe ratios over this sample.

In the paper I show that if returns are normal then the following

approximation holds

$$

\hat{\zeta}\approx\mathcal{N}\left(\zeta,\frac{1}{n}\left(

R + \frac{1}{2}\operatorname{Diag}\left(\zeta\right)\left(R \odot R\right)\operatorname{Diag}\left(\zeta\right)

\right)\right).

$$

There is a more general form for Elliptically distributed returns.

In the paper I find, via simulations, that for realistic

SNRs and large sample sizes, the more general form does not add much

accuracy. In fact, for the small SNRs one is likely to see in practice

the simple approximation

$$

\hat{\zeta}\approx\mathcal{N}\left(\zeta,\frac{1}{n}R\right)

$$

will suffice.

Now note that, under the null hypothesis that $\zeta = \zeta_0$, one has

$$

z = \sqrt{n} \left(R^{1/2}\right)^{-1} \left(\hat{\zeta} - \zeta_0\right) \approx\mathcal{N}\left(0,I\right),

$$

where $R^{1/2}$ is a matrix square root of $R$.

Testing the null hypothesis should proceed by computing (or estimating) the

vector $z$, then comparing to normality, either by a Chi-square statistic,

or performing Bonferroni-corrected normal inference on the largest element.

In the paper I used a simple rank-one model for correlation for simulations

using

$$

R = \left(1-\rho\right) I + \rho 1 1^{\top}.

$$

This effectively models the influence of a common single 'latent' factor.

Certainly this is more flexible for modeling real returns

than assuming identity correlation, but is not terribly realistic.

Under this model of $R$ it is simple enough to compute the inverse-square-root

of $R$. Namely

$$

\left(R^{1/2}\right)^{-1} = \left(1-\rho\right)^{-1/2} I + \frac{1}{p}\left(\frac{1}{\sqrt{1-\rho+p\rho}} - \frac{1}{\sqrt{1-\rho}}\right)1 1^{\top}.

$$

Let's just confirm with code:

p <- 4

rho <- 0.3

R <- (1-rho) * diag(p) + rho

ihR <- (1/sqrt(1-rho)) * diag(p) + (1/p) * ((1/sqrt(1-rho+p*rho)) - (1/sqrt(1-rho)))

hR <- solve(ihR)

R - hR %*% hR

[,1] [,2] [,3] [,4]

[1,] 4.44089e-16 1.66533e-16 1.11022e-16 1.66533e-16

[2,] 1.66533e-16 0.00000e+00 5.55112e-17 5.55112e-17

[3,] 1.66533e-16 1.66533e-16 0.00000e+00 1.11022e-16

[4,] 1.11022e-16 1.11022e-16 1.11022e-16 2.22045e-16

So to test the null hypothesis, one computes

$$

z = \sqrt{n} \left( \left(1-\rho\right)^{-1/2} I + \frac{1}{p}\left(\frac{1}{\sqrt{1-\rho+p\rho}} - \frac{1}{\sqrt{1-\rho}}\right)1 1^{\top} \right)

\left(\hat{\zeta} - \zeta_0\right)

$$

to test against normality. But note that our linear transformation is monotonic (indeed affine):

if $v_i \ge v_j$ and $w = \left(R^{1/2}\right)^{-1} v$, then $w_i \ge w_j$.

This means that the maximum element of $z$ has the same index as the maximum element of

$\hat{\zeta} - \zeta_0$.

To perform Bonferroni correction we need only transform the largest element of

$\hat{\zeta} - \zeta_0$, by scaling it up, and shifting to accomodate the average.

So if the largest element of $\hat{\zeta} - \zeta_0$ is $y$, and the average value

is $a = \frac{1}{p}1^{\top} \left(\hat{\zeta} - \zeta_0\right)$, then the largest

value of $z$ is

$$

\frac{\sqrt{n} y}{\sqrt{1-\rho}} + a \sqrt{n} \left(\frac{1}{\sqrt{1-\rho+p\rho}} - \frac{1}{\sqrt{1-\rho}}\right)

$$

Reject the null hypothesis if this is larger than $\Phi\left(1 - \alpha/p\right)$.

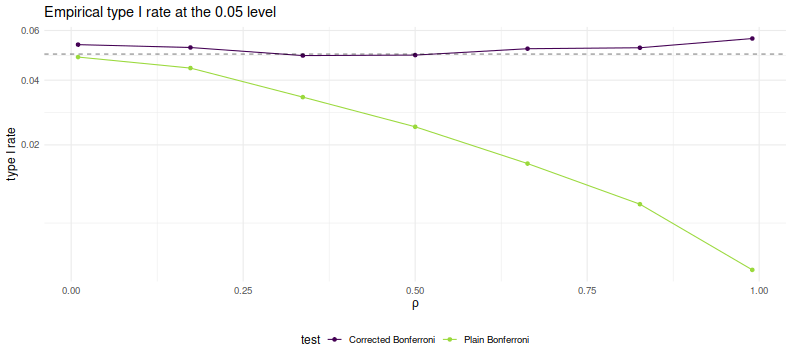

Simulations

Here we perform simple simulations of Bonferroni and corrected Bonferroni.

We will assume that returns are Gaussian, that the correlation follows

our simple rank one form, that the correlation is known in order to perform the

corrected test.

We simulate two years of daily data on 100 assets. For each choice of $\rho$

we perform 10000 simulations under the null of zero SNR, computing the simple and 'improved'

Bonferroni corrected hypothesis tests. We tabulate the empirical type I rate

and plot against $\rho$.

suppressMessages({

library(dplyr)

library(tidyr)

library(future.apply)

})

# set up the functions

rawsim <- function(nday,nlatf,nsim=100,rho=0) {

R <- pmin(diag(nlatf) + rho,1)

mu <- rep(0,nlatf)

apart <- sqrt(nday)/sqrt(1-rho)

bpart <- sqrt(nday) * ((1/sqrt(1-rho+nlatf*rho)) - (1/sqrt(1-rho)))

mhtpvals <- replicate(nsim,{

X <- mvtnorm::rmvnorm(nday,mean=mu,sigma=R)

x <- colMeans(X) / apply(X,2,sd)

bonf_pval <- nlatf * SharpeR::psr(max(x),df=nday-1,zeta=0,ope=1,lower.tail=FALSE)

# do the correction

corr_stat <- apart * max(x) + bpart * mean(x)

corr_pval <- nlatf * pnorm(corr_stat,lower.tail=FALSE)

c(bonf_pval,corr_pval)

})

data_frame(bonf_pvals=as.numeric(mhtpvals[1,]),

corr_pvals=as.numeric(mhtpvals[2,]))

}

many_rawsim <- function(nday,nlatf,rho,nsim=1000L,nnodes=7) {

if ((nsim > 10*nnodes) && require(future.apply)) {

plan(multisession, workers = 7)

nper <- as.numeric(table(1:nsim %% nnodes))

retv <- future_lapply(nper,function(aper) rawsim(nday=nday,nlatf=nlatf,rho=rho,nsim=aper)) %>%

bind_rows()

plan(sequential)

} else {

retv <- rawsim(nday=nday,nlatf=nlatf,rho=rho,nsim=nsim)

}

retv

}

mhtsim <- function(alpha=0.05,...) {

many_rawsim(...) %>%

tidyr::gather(key=method,value=pvalues) %>%

group_by(method) %>%

summarize(rej_rate=mean(pvalues < alpha)) %>%

ungroup() %>%

arrange(method)

}

# perform simulations

nsim <- 10000

nday <- 2*252

nlatf <- 100

params <- data_frame(rho=seq(0.01,0.99,length.out=7))

set.seed(123)

resu <- params %>%

group_by(rho) %>%

summarize(resu=list(mhtsim(nday=nday,nlatf=nlatf,rho=rho,nsim=nsim))) %>%

ungroup() %>%

unnest()

suppressMessages({

library(dplyr)

library(ggplot2)

})

# plot empirical rates:

ph <- resu %>%

mutate(method=gsub('bonf_pvals','Plain Bonferroni',method)) %>%

mutate(method=gsub('corr_pvals','Corrected Bonferroni',method)) %>%

ggplot(aes(rho,rej_rate,color=method)) +

geom_line() + geom_point() +

geom_hline(yintercept=0.05,linetype=2,alpha=0.5) +

scale_y_sqrt() +

labs(title='Empirical type I rate at the 0.05 level',

x=expression(rho),y='type I rate',

color='test')

print(ph)

As desired, we maintain nominal coverage using the correction for $\rho$, while

the naive Bonferroni is too conservative for large $\rho$.

This is not yet a practical test, but could be used for rough estimation by

plugging in the average sample correlation (or just SWAG'ing one).

To my tastes a more interesting question is whether one can

generalize this process to a rank $k$ approximation of $R$ while

keeping the monotonicity property. (I have my doubts this is possible)

Click to read and post comments

May 11, 2019

In a previous blog post we looked at a symmetric

confidence intervals on the Signal-Noise ratio.

That study was motivated by the "opportunistic strategy", wherein

one observes the historical returns of an asset to determine whether

to hold it long or short. Then, conditional on the sign of the trade,

we were able to construct proper confidence intervals on the Signal-Noise

ratio of the opportunistic strategy's returns.

I had hoped that one could generalize from the single asset opportunistic

strategy to the case of $p$ assets, where one constructs the Markowitz

portfolio based on observed returns.

I have not had much luck finding that generalization.

However, we can generalize the opportunistic strategy in a different

way to what I call the "Winner Take All" strategy.

Here one observes the historical returns of $p$ different assets,

then chooses the one with the highest observed Sharpe ratio to hold long.

(Let us hold off on an Opportunistic Winner Take All.)

Observe, however, this is just the problem of inferring the Signal Noise

ratio (SNR) of the asset with the maximal Sharpe.

We previously approached that problem using a

Markowitz approximation, finding it somewhat lacking.

That Markowitz approximation was an attempt to correct some deficiencies

with what is apparently the state of the art in the field, Marcos

Lopez de Prado's (now AQR's?) "Most Important Plot in All of Finance",

which is a thin layer of Multiple Hypothesis Testing correction over the

usual distribution of the Sharpe ratio.

In a previous blog post, we found that

Lopez de Prado's method would have lower than nominal type I rates

as it ignored correlation of assets.

Moreover, a simple MHT correction will not, I think,

deal very well with the case where there are great differences

in the Signal Noise ratios of the assets.

The 'stinker' assets with low SNR will simply spoil our inference,

unlikely to have much influence on which asset shows the

highest Sharpe ratio, and only causing us to increase our

significance threshold.

With my superior googling skills I recently discovered a 2013 paper

by Lee et al,

titled Exact Post-Selection Inference, with Application to the Lasso.

While aimed at the Lasso, this paper includes a procedure that

essentially solves our problem, giving hypothesis tests or

confidence intervals with nominal coverage on the asset with

maximal Sharpe among a set of possibly correlated assets.

The Lee et al paper assumes one observes $p$-vector

$$

y \sim \mathcal{N}\left(\mu,\Sigma\right).

$$

Then conditional on $y$ falling in some polyhedron, $Ay \le b$, we wish

to perform inference on $\nu^{\top}y$.

In our case the polyhedron will be the union of all polyhedra with the same

maximal element of $y$ as we observed.

That is, assume that we have reordered the elements of $y$ such that $y_1$ is the

largest element. Then $A$ will be a column of negative ones, cbinded to the $p-1$ identity

matrix, and $b$ will be a $p-1$ vector of zeros.

The test is defined on $\nu=e_1$ the vector with a single one in the first element

and zero otherwise.

Their method works by decomposing the condition $Ay \le b$ into a condition on

$\nu^{\top}y$ and a condition on some $z$ which is normal but independent of

$\nu^{\top}y$.

You can think of this as kind of inverting the transform by $A$.

After this transform, the value of $\nu^{\top}y$ is restricted to a line

segment, so we need only perform inference on a truncated normal.

The code to implement this is fairly straightforward, and given below.

The procedure to compute the quantile function, which we will need

to compute confidence intervals, is a bit trickier, due to numerical

issues. We give a hacky version below.

# Lee et. al eqn (5.8)

F_fnc <- function(x,a,b,mu=0,sigmasq=1) {

sigma <- sqrt(sigmasq)

phis <- pnorm((c(x,a,b)-mu)/sigma)

(phis[1] - phis[2]) / (phis[3] - phis[2])

}

# Lee eqns (5.4), (5.5), (5.6)

Vfuncs <- function(z,A,b,ccc) {

Az <- A %*% z

Ac <- A %*% ccc

bres <- b - Az

brat <- bres

brat[Ac!=0] <- brat[Ac!=0] / Ac[Ac!=0]

Vminus <- max(brat[Ac < 0])

Vplus <- min(brat[Ac > 0])

Vzero <- min(bres[Ac == 0])

list(Vminus=Vminus,Vplus=Vplus,Vzero=Vzero)

}

# Lee et. al eqn (5.9)

ptn <- function(y,A,b,nu,mu,Sigma,numu=as.numeric(t(nu) %*% mu)) {

Signu <- Sigma %*% nu

nuSnu <- as.numeric(t(nu) %*% Signu)

ccc <- Signu / nuSnu # eqn (5.3)

nuy <- as.numeric(t(nu) %*% y)

zzz <- y - ccc * nuy # eqn (5.2)

Vfs <- Vfuncs(zzz,A,b,ccc)

F_fnc(x=nuy,a=Vfs$Vminus,b=Vfs$Vplus,mu=numu,sigmasq=nuSnu)

}

# invert the ptn function to find nu'mu at a given pval.

citn <- function(p,y,A,b,nu,Sigma) {

Signu <- Sigma %*% nu

nuSnu <- as.numeric(t(nu) %*% Signu)

ccc <- Signu / nuSnu # eqn (5.3)

nuy <- as.numeric(t(nu) %*% y)

zzz <- y - ccc * nuy # eqn (5.2)

Vfs <- Vfuncs(zzz,A,b,ccc)

# you want this, but there are numerical issues:

#f <- function(numu) { F_fnc(x=nuy,a=Vfs$Vminus,b=Vfs$Vplus,mu=numu,sigmasq=nuSnu) - p }

sigma <- sqrt(nuSnu)

f <- function(numu) {

phis <- pnorm((c(nuy,Vfs$Vminus,Vfs$Vplus)-numu)/sigma)

#(phis[1] - phis[2]) - p * (phis[3] - phis[2])

phis[1] - (1-p) * phis[2] - p * phis[3]

}

# this fails sometimes, so find a better interval

intvl <- c(-1,1) # a hack.

# this is very unfortunate

trypnts <- seq(from=min(y),to=max(y),length.out=31)

ys <- sapply(trypnts,f)

dsy <- diff(sign(ys))

if (any(dsy < 0)) {

widx <- which(dsy < 0)

intvl <- trypnts[widx + c(0,1)]

} else {

maby <- 2 * (0.1 + max(abs(y)))

trypnts <- seq(from=-maby,to=maby,length.out=31)

ys <- sapply(trypnts,f)

dsy <- diff(sign(ys))

if (any(dsy < 0)) {

widx <- which(dsy < 0)

intvl <- trypnts[widx + c(0,1)]

}

}

uniroot(f=f,interval=intvl,extendInt='yes')$root

}

Testing on normal data

Here we test the code above on the problem considered in Theorem 5.2 of

Lee et al.

That is, we draw

$y \sim \mathcal{N}\left(\mu,\Sigma\right)$,

then observe the value of $F$ given in Theorem 5.2

when we plug in the actual population values of $\mu$ and $\Sigma$.

This is several steps removed from our problem of inference on

the SNR, but it is best to pause and make sure the implementation

is correct first.

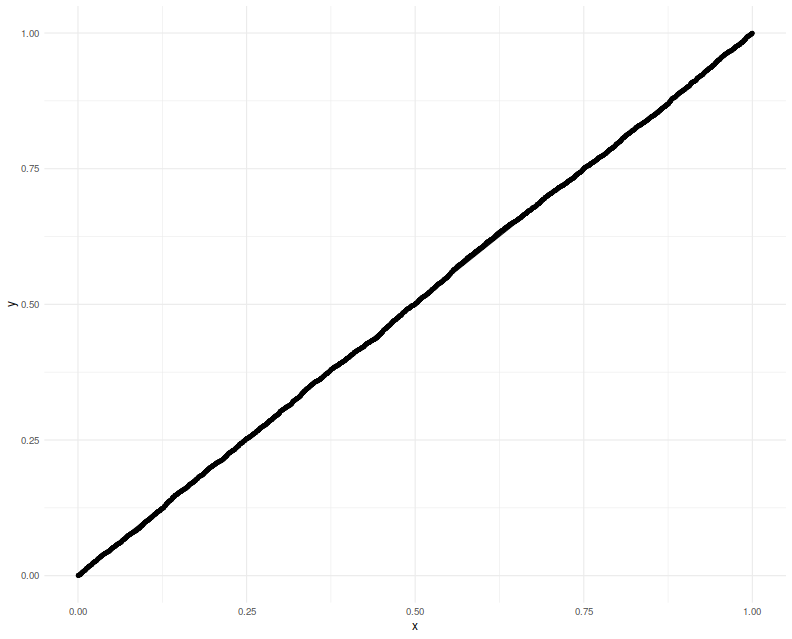

We perform 5000 simulations, letting $p=20$, then creating a random $\mu$ and

$\Sigma$, drawing a single $y$, observing which element is the maximum,

creating $A, b, \nu$, then computing the $F$ function, resulting in

a $p$-value which should be uniform. We Q-Q plot those empirical $p$-values

against a uniform law, finding them on the $y=x$ line.

gram <- function(x) { t(x) %*% x }

rWish <- function(n,p=n,Sigma=diag(p)) {

require(mvtnorm)

gram(rmvnorm(p,sigma=Sigma))

}

nsim <- 5000

p <- 20

A1 <- cbind(-1,diag(p-1))

set.seed(1234)

pvals <- replicate(nsim,{

mu <- rnorm(p)

Sigma <- rWish(n=2*p+5,p=p)

y <- t(rmvnorm(1,mean=mu,sigma=Sigma) )

# collect the maximum, so reorder the A above

yord <- order(y,decreasing=TRUE)

revo <- seq_len(p)

revo[yord] <- revo

A <- A1[,revo]

nu <- rep(0,p)

nu[yord[1]] <- 1

b <- rep(0,p-1)

foo <- ptn(y=y,A=A,b=b,nu=nu,mu=mu,Sigma=Sigma)

})

# plot them:

library(dplyr)

library(ggplot2)

ph <- data_frame(pvals=pvals) %>%

ggplot(aes(sample=pvals)) +

geom_qq(distribution=stats::qunif) +

geom_qq_line(distribution=stats::qunif)

print(ph)

Now we attempt to use the confidence interval code. We construct

a one-sided 95% confidence interval, and check how often it is violated

by the $\mu$ of the element which shows the highest $y$. We will

find that the empirical rate of violations of our confidence interval

is indeed around 5%:

nsim <- 5000

p <- 20

A1 <- cbind(-1,diag(p-1))

set.seed(1234)

tgtval <- 0.95

viols <- replicate(nsim,{

mu <- rnorm(p)

Sigma <- rWish(n=2*p+5,p=p)

y <- t(rmvnorm(1,mean=mu,sigma=Sigma) )

# collect the maximum, so reorder the A above

yord <- order(y,decreasing=TRUE)

revo <- seq_len(p)

revo[yord] <- revo

A <- A1[,revo]

nu <- rep(0,p)

nu[yord[1]] <- 1

b <- rep(0,p-1)

# mu is unknown to this guy

foo <- citn(p=tgtval,y=y,A=A,b=b,nu=nu,Sigma=Sigma)

violated <- mu[yord[1]] < foo

})

print(sprintf('%.2f%%',100*mean(viols)))

Testing on the Sharpe ratio

To use this machinery to perform inference on the SNR, we can either port

the results to the multivariate $t$-distribution,

which seems unlikely because uncorrelated marginals of a multivariate

$t$ are not independent.

Instead we lean on the normal approximation to the vector of Sharpe ratios.

If the $p$-vector $x$ is normal with correlation matrix $R$, then

$$

\hat{\zeta}\approx\mathcal{N}\left(\zeta,\frac{1}{n}\left(

R + \frac{1}{2}\operatorname{Diag}\left(\zeta\right)\left(R \odot R\right)\operatorname{Diag}\left(\zeta\right)

\right)\right),

$$

where $\hat{\zeta}$ is the $p$-vector of Sharpe ratios

computed by observing $n$ independent draws of $x$, and

$\zeta$ is the $p$-vector of Signal Noise ratios.

Note how this generalizes the 'Lo' form of the standard

error of a scalar Sharpe ratio, viz

$\sqrt{(1 + \zeta^2/2)/n}$.

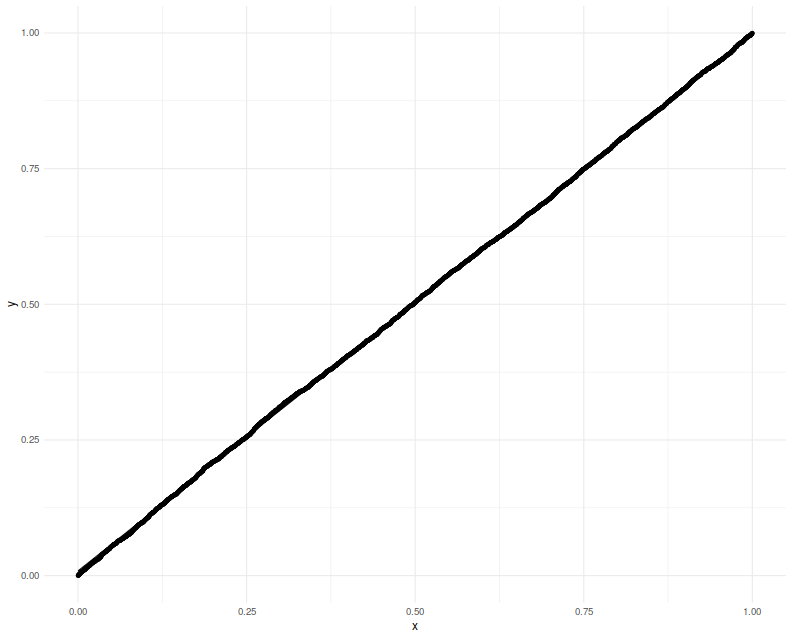

Here we will check the uniformity of $p$ values resulting from

using this normal approximation. This is closer to the actual

inference we want to do, except we will cheat by using the actual $R$ and $\zeta$

to construct what is essentially the $\Sigma$ to Lee's formulation.

We will set $p=20$ and draw 3 years of daily data.

Again we plot the putative $p$-values against uniformity

and find a good match.

# let's test it!

nsim <- 5000

p <- 20

ndays <- 3 * 252

A1 <- cbind(-1,diag(p-1))

set.seed(4321)

pvals <- replicate(nsim,{

# population values here

mu <- rnorm(p)

Sigma <- rWish(n=2*p+5,p=p)

RRR <- cov2cor(Sigma)

zeta <- mu /sqrt(diag(Sigma))

Xrets <- rmvnorm(ndays,mean=mu,sigma=Sigma)

srs <- colMeans(Xrets) / apply(Xrets,2,FUN=sd)

y <- srs

mymu <- zeta

mySigma <- (1/ndays) * (RRR + (1/2) * diag(zeta) %*% (RRR * RRR) %*% diag(zeta))

# collect the maximum, so reorder the A above

yord <- order(y,decreasing=TRUE)

revo <- seq_len(p)

revo[yord] <- revo

A <- A1[,revo]

nu <- rep(0,p)

nu[yord[1]] <- 1

b <- rep(0,p-1)

foo <- ptn(y=y,A=A,b=b,nu=nu,mu=mymu,Sigma=mySigma)

})

# plot them:

library(dplyr)

library(ggplot2)

ph <- data_frame(pvals=pvals) %>%

ggplot(aes(sample=pvals)) +

geom_qq(distribution=stats::qunif) +

geom_qq_line(distribution=stats::qunif)

print(ph)

Lastly we make one more modification, filling in

sample estimates for $\zeta$ and $R$ into the computation

of the covariance.

We compute

one-sided 95% confidence intervals, and check how the empirical

rate of violations.

We find the rate to be around 5%.

nsim <- 5000

p <- 20

ndays <- 3 * 252

A1 <- cbind(-1,diag(p-1))

set.seed(9873) # 5678 gives exactly 250 / 5000, which is eerie

tgtval <- 0.95

viols <- replicate(nsim,{

# population values here

mu <- rnorm(p)

Sigma <- rWish(n=2*p+5,p=p)

RRR <- cov2cor(Sigma)

zeta <- mu /sqrt(diag(Sigma))

Xrets <- rmvnorm(ndays,mean=mu,sigma=Sigma)

srs <- colMeans(Xrets) / apply(Xrets,2,FUN=sd)

Sighat <- cov(Xrets)

Rhat <- cov2cor(Sighat)

y <- srs

# now use the sample approximations.

# you can compute this from the observed information.

mySigma <- (1/ndays) * (Rhat + (1/2) * diag(srs) %*% (Rhat * Rhat) %*% diag(srs))

# collect the maximum, so reorder the A above

yord <- order(y,decreasing=TRUE)

revo <- seq_len(p)

revo[yord] <- revo

A <- A1[,revo]

nu <- rep(0,p)

nu[yord[1]] <- 1

b <- rep(0,p-1)

# mu is unknown to this guy

foo <- citn(p=tgtval,y=y,A=A,b=b,nu=nu,Sigma=mySigma)

violated <- zeta[yord[1]] < foo

})

print(sprintf('%.2f%%',100*mean(viols)))

Putting it together

Lee's method appears to give nominal coverage for hypothesis tests and confidence

intervals on the SNR of the asset with maximal Sharpe.

In principle it should not be affected by correlation of the assets

or by large differences in the SNRs of the assets.

It should be applicable in the $p > n$ case, as we are not inverting

the covariance matrix.

On the negative side, requiring one estimate the correlation of assets

for the computation will not scale with large $p$.

We are guardedly optimistic that this method is not adversely affected by the

normal approximation of the Sharpe ratio,

although it would be ill-advised to use it for the case of small samples

until more study is performed.

Moreover the quantile function we hacked together here should be improved

for stability and accuracy.

Click to read and post comments

Mar 17, 2019

Consider the problem of computing confidence intervals on the Signal-Noise

ratio, which is the population quantity $\zeta = \mu/\sigma$,

based on the observed Sharpe ratio $\hat{\zeta} = \hat{\mu}/\hat{\sigma}$.

If returns are Gaussian, one can compute 'exact' confidence intervals

by inverting the CDF of the non-central $t$ distribution with respect

to its parameter.

Typically instead one often uses an approximate standard error, using

either the formula published by Johnson & Welch (and much later by Andrew Lo),

or one using higher order moments given by Mertens, then constructs

Wald-test confidence intervals.

Using standard errors yields symmetric intervals of the

form

$$

\hat{\zeta} \pm z_{\alpha/2} s,

$$

where $s$ is the approximate standard error, and $z_{\alpha/2}$ is the normal $\alpha/2$ quantile.

As typically constructed, the 'exact' confidence intervals based on the non-central $t$

distributionare not symmetric in general, but are very close, and can be made

symmetric. The symmetry condition can be expressed as

$$

\mathcal{P}\left(|\zeta - \hat{\zeta}| \ge c\right) = \alpha,

$$

where $c$ is some constant.

Picking sides

Usually I think of the Sharpe ratio as a tool to answer the

question:

Should I invest a predetermined amount of capital (long) in this asset?

The Sharpe ratio can be used to construct confidence intervals

on the Signal-Noise ratio to help answer that question.

Pretend instead that you are more opportunistic: instead of considering

a predetermined side to the trade, you will observe historical returns

of the asset. Then if the Sharpe ratio is positive, you will consider investing

in the asset, and if the Sharpe is negative, you will consider shorting the

asset. Can we rely on our standard confidence intervals now? After all,

we are now trying to perform inference on

$\operatorname{sign}\left(\hat{\zeta}\right) \zeta$, which is not a population

quantity. Rather it mixes up the population Signal-Noise ratio with

information from the observed sample (the sign of the Sharpe).

(Because of this mixing of a population quantity with information from

the sample, real statisticians

get a bit indignant

when you try to call this a "confidence interval". So don't do that.)

It turns out that you can easily adapt the symmetric confidence intervals

to this problem. Because you can multiply

the inside of $\left|\zeta - \hat{\zeta}\right|$ by $\pm 1$ without

affecting the absolute value, we have

$$

\left|\zeta - \hat{\zeta}\right| \ge c \Leftrightarrow

\left| \operatorname{sign}\left(\hat{\zeta}\right) \zeta - \left|\hat{\zeta}\right|\right| \ge c.

$$

Thus

$$

\left|\hat{\zeta}\right| \pm z_{\alpha/2} s

$$

are $1-\alpha$ confidence intervals on

$\operatorname{sign}\left(\hat{\zeta}\right) \zeta$.

Although the type I error rate is maintained, the 'violations' of the

confidence interval can be asymmetric.

When the Signal Noise ratio is large (in absolute value), type I errors

tend to occur on both sides of the confidence interval equally, because

the Sharpe is usually the same sign as the Signal-Noise ratio.

When the Signal-Noise ratio is near zero, however, typically the type I

errors occur only on the lower side.

(This must be the case when the Signal-Noise ratio is exactly zero.)

Of course, since the Signal-Noise ratio is the unknown population parameter,

you do not know which situation you are in, although you have some

hints from the observed Sharpe ratio.

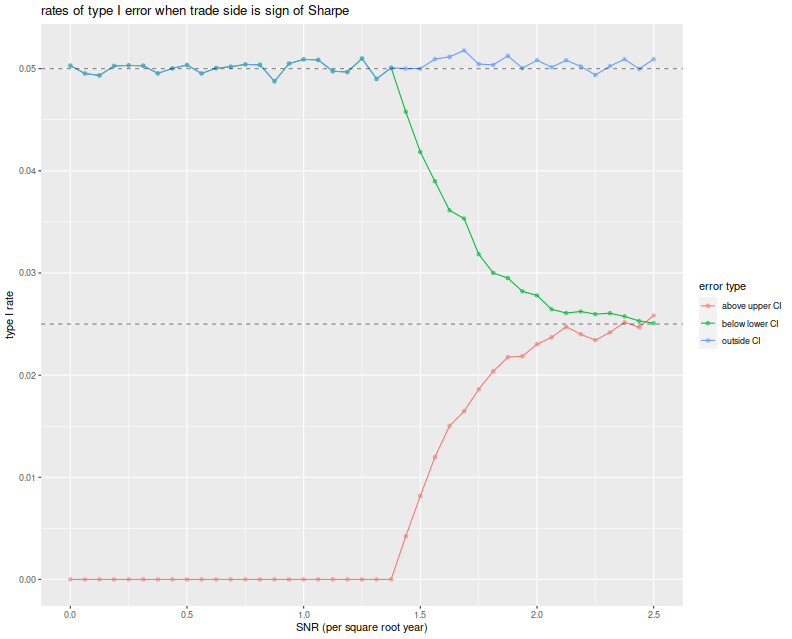

Before moving on, here we test the symmetric confidence intervals.

We vary the Signal Noise ratio from 0 to 2.5 in 'annual units',

draw two years of daily normal returns with that Signal-Noise ratio,

pick a side of the trade based on the sign of the Sharpe ratio,

then build symmetric confidence intervals using the standard

error estimator $\sqrt{(1 + \hat{\zeta}^2/2)/n}$.

We build the 95% confidence intervals, then note any

breaches of the upper and lower confidence bounds.

We repeat this 10000 times for each choice of SNR.

We then plot the type I rate for the lower bound of the CI, the upper

bound and the total type I rate, versus the Signal Noise ratio.

We see that the total empirical type I rate is very near the nominal

rate of 5%, and this is entirely attributable to violations of

the lower bound up until a Signal Noise ratio of around 1.4 per

square root year. At around 2.5 per square root year, the type I errors

are observed in equal proportion on both sides of the CI.

suppressMessages({

library(dplyr)

library(tidyr)

library(future.apply)

})

# run one simulation of normal returns and CI violations

onesim <- function(n,pzeta,zalpha=qnorm(0.025)) {

x <- rnorm(n,mean=pzeta,sd=1)

sr <- mean(x) / sd(x)

se <- sqrt((1+0.5*sr^2)/n)

cis <- abs(sr) + se * abs(zalpha) * c(-1,1)

pquant <- sign(sr) * pzeta

violations <- c(pquant < cis[1],pquant > cis[2])

}

# do a bunch of sims, then sum the violations of low and high;

repsim <- function(nrep,n,pzeta,zalpha) {

jumble <- replicate(nrep,onesim(n=n,pzeta=pzeta,zalpha=zalpha))

retv <- t(jumble)

colnames(retv) <- c('nlo','nhi')

retv <- as.data.frame(retv) %>%

summarize_all(.funs=sum)

retv$nrep <- nrep

invisible(retv)

}

manysim <- function(nrep,n,pzeta,zalpha,nnodes=7) {

if (nrep > 2*nnodes) {

plan(multisession, workers = 7)

# do in parallel.

nper <- table(1 + ((0:(nrep-1) %% nnodes)))

retv <- future_lapply(nper,function(aper) repsim(nrep=aper,n=n,pzeta=pzeta,zalpha=zalpha)) %>%

bind_rows() %>%

summarize_all(.funs=sum)

plan(sequential)

} else {

retv <- repsim(nrep=nrep,n=n,pzeta=pzeta,zalpha=zalpha)

}

# turn sums into means

retv %>%

mutate(vlo=nlo/nrep,vhi=nhi/nrep) %>%

dplyr::select(vlo,vhi)

}

# run a bunch

ope <- 252

nyr <- 2

alpha <- 0.05

# simulation params

params <- data_frame(zetayr=seq(0,2.5,by=0.0625)) %>%

mutate(pzeta=zetayr/sqrt(ope)) %>%

mutate(n=round(ope*nyr))

# run a bunch

nrep <- 100000

set.seed(4321)

system.time({

results <- params %>%

group_by(zetayr,pzeta,n) %>%

summarize(sims=list(manysim(nrep=nrep,nnodes=7,

pzeta=pzeta,n=n,zalpha=qnorm(alpha/2)))) %>%

ungroup() %>%

tidyr::unnest()

})

suppressMessages({

library(dplyr)

library(tidyr)

library(ggplot2)

})

ph <- results %>%

mutate(vtot=vlo+vhi) %>%

gather(key=series,value=violations,vlo,vhi,vtot) %>%

mutate(series=case_when(.$series=='vlo' ~ 'below lower CI',

.$series=='vhi' ~ 'above upper CI',

.$series=='vtot' ~ 'outside CI',

TRUE ~ 'error')) %>%

ggplot(aes(zetayr, violations, colour=series)) +

geom_line() + geom_point(alpha=0.5) +

geom_hline(yintercept=c(alpha/2,alpha),linetype=2,alpha=0.5) +

labs(x='SNR (per square root year)',y='type I rate',

color='error type',title='Rates of type I error when trade side is sign of Sharpe')

print(ph)

A Bayesian Donut?

Of course, this strategy seems a bit unrealistic:

what's the point of constructing confidence intervals if you are

going to trade the asset no matter what the evidence?

Instead, consider a fund manager whose trading strategies are

all above average: she/he observes the Sharpe ratio of a backtest,

then only trades a strategy if $|\hat{\zeta}| \ge c$ for some sufficiently

large $c$, and picks a side based on $\operatorname{sign}\left(\hat{\zeta}\right)$.

This is a 'donut'.

Conditional on observing $|\hat{\zeta}| \ge c$, can one construct

a reliable confidence interval on

$\operatorname{sign}\left(\hat{\zeta}\right) \zeta$?

Perhaps our fund manager thinks there is no point in doing so if $c$

is sufficiently large.

I think to do so you have to make some assumptions about the distribution of $\zeta$

and rely on Baye's law.

We did not say what would happen if the junior quant at this shop

developed a strategy where $|\hat{\zeta}| < c$, but presumably

the junior quants were told to keep working until they beat the magic

threshold.

If the junior quants only produce strategies with small $\zeta$, one

suspects that the $c$ threshold does very little to reject bad

strategies, rather it just slows down their deployment.

(In response the quants will surely beef up their backtesting

infrastructure, or invent automatic strategy generation.)

Generalizing to higher dimensions

The real interesting question is what this looks like in higher dimensions.

Now one observes $p$ assets, and is to construct a portfolio

on those assets. Can we construct good confidence intervals on the

Sharpe ratio of the chosen portfolio?

In this setting we have many more possible choices, so a general

purpose analysis seems unlikely.

However, if we restrict ourselves to the Markowitz portfolio,

I suspect some progress can be made.

(Although I have been very slow to make it!)

I hope to purse this in a followup blog post.

Click to read and post comments